INTRODUCTION

The intensification of digital transformation in recent decades has highlighted the centrality of global product platforms as engines of economic growth and continuous innovation. In this context, the fintechs and Software as a Service (SaaS) sectors play a leading role in redefining business models and shaping dynamic, competitive, and regulated digital ecosystems. Artificial intelligence (AI) emerges in this scenario not only as a technological support tool but as a strategic element capable of transforming the lifecycle of digital products, expanding their scalability, adaptability, and economic impact across different regions of the world (McKinsey, 2023).

The theme is justified by the growing relevance of AI as a resource to sustain innovation on a global scale, considering that, according to the World Economic Forum (2022), technologies based on artificial intelligence are now considered essential for the competitiveness of organizations operating in multiple markets. In sectors such as fintechs and SaaS, complexity increases due to distinct regulatory environments and the competitive pressures from both local and global players, requiring companies to align compliance, governance, and disruptive innovation in their digital products.

The research problem guiding this work consists of understanding how the strategic application of artificial intelligence can drive scalable innovation in global digital platforms, particularly in the fintechs and SaaS sectors. The hypothesis is that AI, when integrated into the product lifecycle, can accelerate innovation, increase operational efficiency, and enhance the ability to adapt to different regulatory and cultural contexts, thereby becoming a sustainable competitive differentiator.

The general objective of this article is to demonstrate how the strategic application of artificial intelligence can drive scalable innovation in global digital products. To achieve this goal, three specific objectives were defined: to identify ways of integrating AI into the lifecycle of digital products to generate business impact; to analyze scalability strategies in different regulatory environments, considering Brazil, Europe, and global markets; and to discuss the importance of multidisciplinary and data-driven leadership in the success of AI-embedded products.

The scope of this study focuses on the fintechs and SaaS sectors, as they represent environments of continuous innovation and rapid growth on a global scale. The research adopts a bibliographic and documentary review methodology, encompassing classical authors such as Christensen (2013), Ries (2011), Tidd and Bessant (2015), and Andrew Ng (2018), in addition to recent reports published by institutions such as McKinsey, the Boston Consulting Group, and the World Economic Forum. This approach makes it possible to relate theoretical foundations of innovation and strategic management with empirical data on market practices, in order to build a critical and applied analysis.

The structure of the article is organized as follows: first, the theoretical framework is presented, with emphasis on the concepts of scalable innovation, innovation management frameworks, and recent contributions on artificial intelligence applied to digital products. Next, the methodology is presented, explaining the nature, approach, and technical procedures of the research. Then, the results and discussions outline scalable innovation strategies adopted by fintechs and SaaS companies, comparing practices and highlighting critical success factors. Finally, the concluding remarks synthesize the main findings and propose practical and academic contributions, followed by recommendations for future research.

THEORETICAL FRAMEWORK

The phenomenon of scalable innovation in global digital products has been widely studied from different perspectives, ranging from the theoretical frameworks of innovation management to contemporary debates on artificial intelligence and technological regulation. The need to understand the mechanisms that sustain exponential growth in sectors such as fintechs and Software as a Service (SaaS) makes it essential to foster dialogue between academic tradition and recent market evidence.

For Christensen (2013), disruptive innovation represents not only a challenge for established organizations but also an opportunity to reconstruct entire ecosystems, forcing companies to rethink their models of value creation and capture. In this sense, the incorporation of artificial intelligence into the lifecycle of digital products can be interpreted as the contemporary expression of this dilemma, since it simultaneously imposes risks and opportunities for corporations operating in multiple markets.

Tidd and Bessant (2015) reinforce that innovation must be understood as a systemic process, which articulates technological, organizational, and social dimensions. Scalability, in turn, emerges when this process can be replicated in different institutional contexts without loss of efficiency.

This conception aligns with McKinsey’s (2023) reports, which indicate that companies aligning AI with structured innovation frameworks can sustain growth rates up to three times higher than their competitors. Thus, the literature suggests that scalable innovation cannot be reduced to isolated technical advances but must be interpreted as the result of the integration between technology, strategic management, and regulatory governance.

SCALABLE INNOVATION AND GLOBAL PLATFORMS

Scalable innovation differs from traditional processes by multiplying globally without proportional increases in resources. According to Tidd and Bessant (2015, p. 32):

Innovation is a process that requires discipline, methods, and structures. It is not merely about generating creative ideas but about organizing them in such a way as to produce results that can be continuously applied and replicated in different contexts.

In the case of digital platforms, this characteristic is amplified, since cloud-based products can be distributed worldwide with reduced marginal costs. The World Economic Forum (2022) emphasizes that global competitiveness depends not only on the creation of new products but also on the ability to scale them in fragmented regulatory environments, ensuring technical interoperability and cultural acceptance. Thus, scalability does not translate solely into growth, but into long-term strategic sustainability.

ARTIFICIAL INTELLIGENCE AS A DRIVER OF SCALABILITY

Recent literature points to AI as the main driver of scalable innovation. Andrew Ng (2018) coined the metaphor that “artificial intelligence is the new electricity,” suggesting that, just as electricity transformed entire industries, AI has the potential to redefine all productive sectors. This perspective demonstrates its transversality, as it is not limited to a specific field but permeates sectors ranging from healthcare and finance to education and manufacturing.

McKinsey (2023) presents data that reinforce this vision: organizations that implemented AI in their product development processes reported average gains of 20% in operational efficiency and increases of up to 15% in customer retention rates, especially in digital platforms. However, these benefits are not automatic. The Boston Consulting Group (2023) warns that implementing AI without robust governance mechanisms tends to generate risks of algorithmic bias and losses in consumer trust.

This debate broadens the understanding of scalability. It is not enough for a product to grow in the number of users or geographic reach; such growth must also be sustainable, ethical, and regulatorily accepted. Success, therefore, depends on the integration of technical capability, strategic management, and social legitimacy.

EXPERIENCES IN FINTECHSS: PERSONALIZATION, RISK, AND TRUSTWORTHINESS

The financial sector is paradigmatic for understanding the potential and limitations of AI. Christensen (2013) explains that disruption occurs when new technologies make it possible to serve segments ignored by incumbents, offering more accessible and scalable solutions. fintechss embody this phenomenon precisely, as they use AI to democratize credit, personalize services, and optimize operations in traditionally concentrated environments.

A study by Mastercard (2022) shows that AI-based fraud detection algorithms reduced digital fraud attempts by 30%, while simultaneously preserving a smooth customer experience. This confirms that applying AI in fintechss not only increases operational efficiency but also strengthens consumer trust, which is essential for scalability at a global level.

The future of fintechss will depend on the ability to apply emerging technologies responsibly, ensuring that innovation and regulation progress together to secure consumer trust (Mastercard, 2022, p. 17).

Thus, AI applied to fintechss reveals itself not merely as an innovation tool but as an infrastructure of institutional legitimacy, since it makes it possible to reconcile financial inclusion, regulatory efficiency, and large-scale trustworthiness.

SAAS AND THE CULTURE OF EXPONENTIAL GROWTH

The SaaS (Software as a Service) model has become one of the most fertile environments for incorporating AI on a global scale. Ries (2011) argues that the logic of the Lean Startup, based on rapid cycles of experimentation, validated learning, and continuous iteration, is fundamental for the development of successful digital products. This philosophy is connected to SaaS, where the product is never static but constantly updated, allowing continuous adaptations based on user feedback.

According to the World Economic Forum (2022), the SaaS market is expected to exceed 700 billion dollars by 2030, driven by the integration of AI in automated customer service, personalized recommendation, and optimization of internal workflows. This forecast is not limited to quantitative growth but signals a qualitative change in the way software is conceived, distributed, and scaled.

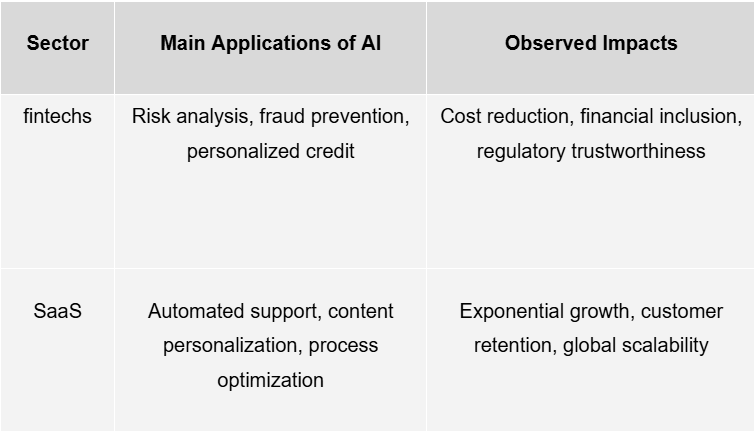

Comparative Table 1 – Applications of AI in fintechss and SaaS

Source: Developed from McKinsey (2023), Mastercard (2022), and WEF (2022).

This Table shows that, although areas of application vary, the final outcome converges: AI expands the ability to scale innovation in a sustainable and replicable way, transforming business models and raising barriers to entry for competitors.

ETHICAL, REGULATORY, AND GOVERNANCE CHALLENGES OF AI

Despite the transformative potential of AI, ethical and regulatory challenges are inescapable. The European Union’s AI Act establishes risk classifications for AI applications and defines requirements for transparency and traceability, setting a pioneering regulatory milestone. In Brazil, the General Data Protection Law (LGPD) represents progress in protecting sensitive information, but the debate on AI still lacks institutional robustness.

According to the World Economic Forum (2023, p. 12):

The scalability of artificial intelligence cannot be assessed solely in terms of efficiency or profitability but must also consider the social and regulatory legitimacy of its adoption.

This perspective reinforces the idea that large-scale technological innovation must be accompanied by mechanisms of trust and accountability. Tidd and Bessant (2015) had already warned that innovation is a phenomenon conditioned by social and institutional factors, and not only by technological advances. Therefore, for AI to sustain scalable innovation, it must be integrated into ethical, regulatory, and governance frameworks capable of legitimizing its use on a global scale.

METHODOLOGY

Methodology is the foundation that guides the logical and operational structure of scientific research, ensuring its validity and reliability. This chapter presents the methodological elements that support the study, including the nature of the research, approach, objectives, technical procedures, universe and sample, data collection and analysis procedures, limitations, and ethical aspects.

NATURE OF THE RESEARCH

The research is characterized as qualitative, as it seeks to understand complex phenomena related to scalable innovation mediated by artificial intelligence, within the context of global digital platforms.

According to Minayo (2014), qualitative research is appropriate for investigating social and organizational phenomena in depth, considering meanings, practices, and interactions that cannot be reduced to numerical indicators.

The focus lies on the critical interpretation of theoretical and documentary data, seeking to understand how AI can be strategically applied to drive innovation in specific sectors, such as fintechs and SaaS. This qualitative nature is justified by the complexity of the phenomenon under study, which involves multiple variables, such as regulation, organizational culture, technological governance, and data-driven leadership.

APPROACH

The study adopts a bibliographic and documentary approach, integrating the analysis of established academic works with the interpretation of technical and institutional reports from companies and international organizations.

According to Lakatos and Marconi (2021), bibliographic research enables the consolidation of existing knowledge on a given subject, while documentary research allows for the analysis of primary or secondary data from institutional or corporate sources.

This mixed approach makes it possible to combine theoretical foundations with practical evidence, enabling the construction of a critical and applied analysis. Reference books were used, such as those by Christensen (2013), Ries (2011), Tidd and Bessant (2015), and Andrew Ng (2018), as well as reports from McKinsey, the Boston Consulting Group, the World Economic Forum, and Mastercard, between 2018 and 2024.

OBJECTIVES

The research has descriptive and explanatory objectives. It is descriptive because it seeks to systematically present the strategies by which artificial intelligence has been applied in the development and scalability of global digital products. It is explanatory because it aims to understand the factors conditioning this process, including regulatory, technological, and organizational variables.

According to Gil (2019, p. 27):

Descriptive research seeks to identify, record, and analyze the characteristics of phenomena without manipulating them, whereas explanatory research aims to understand their causes and effects.

Thus, combining both types of objectives is appropriate to the scope of the study, which requires both detailed description and critical interpretation of the data.

TECHNICAL PROCEDURES

The study adopts bibliographic review and documentary analysis as technical procedures. The bibliographic review involved consulting books, scientific articles, and specialized publications by classical and contemporary authors addressing innovation, AI, and digital platforms.

Documentary analysis was applied to technical and institutional reports from global reference companies in fintechs and SaaS, such as Mastercard, Salesforce, Stripe, Zoom, and Nubank, as well as documents issued by organizations such as the World Economic Forum.

These documents were selected based on criteria of relevance, timeliness, and credibility. Materials published between 2018 and 2024 were prioritized, as this period represents the peak of strategic adoption of AI in these sectors.

UNIVERSE AND SAMPLE

The research universe encompasses global organizations operating in the fintechs and SaaS sectors, focusing on digital platforms that use artificial intelligence as a strategic innovation component.

The sample was defined intentionally and non-probabilistically, selecting paradigmatic cases documented in technical reports and specialized literature.

Intentional sampling is appropriate when seeking to analyze representative and relevant experiences for the research object, as Sampieri et al. (2013) argue, since it allows the selection of units of analysis that best illustrate the phenomenon under investigation.

DATA COLLECTION AND ANALYSIS PROCEDURES

Data collection was carried out in two stages. The first consisted of a bibliographic survey in academic databases such as Scopus and Web of Science, as well as reference books and articles. The second stage involved documentary analysis of publicly available technical and institutional reports.

The documents were organized into thematic categories corresponding to the central axes of the study: integration of AI into the product lifecycle, scalability strategies in different regulatory environments, and multidisciplinary data-driven leadership.

Data analysis followed the technique of content analysis, as proposed by Bardin (2016), which allows the interpretation of explicit and implicit meanings in texts. According to the author:

Content analysis is a set of techniques for analyzing communications, aimed at obtaining, through systematic and objective procedures for describing message content, indicators that allow the inference of knowledge regarding the conditions of production and reception of these messages (Bardin, 2016, p. 48).

This technique enables the articulation between theory and practice, allowing the identification of patterns, contradictions, and trends in the use of AI as a driver of scalable innovation in global digital platforms.

RESEARCH LIMITATIONS

The main limitation of this study lies in the absence of primary data collection, such as interviews or field observations. The choice for secondary sources was deliberate to ensure focus on theoretical and documentary analysis, which does not compromise the validity of the research but limits its capacity for empirical generalization.

Another limitation refers to the rapid pace of technological evolution in the field of artificial intelligence. As new tools and regulations continually emerge, the results presented reflect the state of the art until 2024, but may be surpassed by new evidence in the short term.

ETHICAL ASPECTS

All methodological procedures adopted observed strict ethical standards. The research used exclusively publicly available or institutionally authorized sources, fully respecting copyright and the intellectual integrity of the authors.

In addition, sensitive or confidential data were avoided, ensuring compliance with the principles of ethics in scientific research. As established by Resolution No. 510/2016 of the Brazilian National Health Council, studies that use only publicly accessible secondary data do not require submission to ethics committees, provided they do not involve subject identification or the use of sensitive information.

PRESENTATION AND ANALYSIS OF RESULTS

The analysis of results provides a deeper understanding of how artificial intelligence, when strategically applied, has consolidated itself as a central element in the scalable innovation of global digital platforms. This chapter, structured into four sections, seeks to articulate classical and contemporary literature with documentary data and recent technical reports, examining the experiences of reference companies in the fintechs and Software as a Service (SaaS) sectors.

The starting point is the recognition that AI is no longer a peripheral resource but occupies the center of competitive differentiation strategies. McKinsey (2023) shows that organizations integrating artificial intelligence into their product development cycles achieve average growth twice as high as that of peers who do not use it systematically.

This is a significant finding, as it demonstrates that scalability does not result solely from investments in technological infrastructure but from the ability to articulate continuous innovation, regulatory governance, and organizational leadership.

Classical literature helps interpret these findings. Christensen (2013), when discussing the innovator’s dilemma, emphasizes that established companies fail in the face of disruptions because they become prisoners of their own business models, prioritizing immediate profitability over experimenting with new solutions. This analysis remains current and applies to the contemporary scenario, in which fintechss and SaaS companies challenge incumbent giants through the large-scale application of AI.

At the same time, Ries (2011) reinforces that scalable innovation can only be sustained when anchored in cycles of validated learning and objective metrics, making the product a living organism in constant adaptation.

SCALABLE INNOVATION STRATEGIES IN FINTECHSS

fintechss represent paradigmatic cases of applying AI to scalable innovation, especially because they operate in a highly regulated and sensitive sector: finance. Mastercard (2022), in a technical report, identified that the implementation of fraud detection algorithms made it possible to reduce digital fraud attempts by up to 30% without compromising customer experience.

These data confirm that AI not only improves operational efficiency but also reinforces consumer trust, an essential element in a sector where credibility is synonymous with survival.

The logic of disruption explained by Christensen (2013) becomes evident in this context. According to the author:

Established companies fail to adopt disruptive technologies because their performance metrics and decision-making structures are shaped to preserve already consolidated models, rather than to meet the emerging needs of new market segments (Christensen, 2013, p. 55).

This explanation directly connects to the rise of fintechss, which served niches overlooked by traditional banks by using AI to expand financial inclusion. Nubank, in Brazil, exemplifies this movement by developing proprietary AI-based credit analysis models, which enabled the provision of services to low-income clients or those without robust banking history, consolidating its position as the largest independent digital bank in Latin America.

Globally, Revolut and Stripe have adopted similar strategies. Revolut uses machine learning algorithms for money laundering detection and personalized service offerings to customers in multiple countries, reconciling scalability with regulatory compliance. Stripe, in turn, incorporated AI into its digital payment systems to reduce fraud risk and optimize transactional flows on a global scale. These examples confirm that AI, when integrated into the core of product strategy, becomes a sine qua non condition for sustainable expansion in competitive and regulated environments.

SCALABLE INNOVATION STRATEGIES IN SAAS

The SaaS sector presents itself as a privileged field for analyzing scalability, since its cloud-based architecture allows innovation to be distributed almost instantly on a global scale. The integration of AI into this model further enhances the ability of products to adapt continuously. Ries (2011) argues that the logic of the Lean Startup is particularly relevant in this context, since SaaS operates in short development, feedback, and iteration cycles.

Salesforce, Slack, and Zoom are emblematic examples. Salesforce incorporated AI into its Einstein module, offering sales forecasting and automated recommendation features that significantly increased sales team productivity across companies of different sizes. Slack, in turn, developed recommendation algorithms to suggest relevant channels and prioritize critical messages, optimizing communication for globally distributed teams. After the pandemic, Zoom integrated AI into automatic captioning, engagement analysis, and video optimization features, ensuring scalability in a scenario of exponential user growth.

Data from McKinsey (2023) confirm that SaaS companies incorporating AI into their product cycles achieve increases of up to 25% in customer retention, along with significant reductions in operational costs. This reinforces the argument that scalability in SaaS does not depend only on expanding the user base but also on sustaining high levels of perceived customer value over time.

CROSS-SECTOR COMPARISON: LESSONS LEARNED

Comparing fintechss and SaaS makes it possible to identify relevant convergences and divergences in the application of AI to scalable innovation. Both sectors use AI as a driver of mass personalization, but while fintechss face highly restrictive regulatory environments, SaaS companies deal with pressures of cultural adaptation and global competition.

The World Economic Forum (2022) highlights that consumer trust in digital platforms depends as much on technological effectiveness as on the transparency of regulatory and organizational processes. In this sense, fintechss must ensure the integrity of financial transactions and compliance with local legislation, such as Brazil’s LGPD and the European Union’s GDPR. In SaaS, however, the greater challenge lies in adapting products to different organizational cultures without losing scalability and global consistency.

Table 2 – Critical factors of scalable innovation in fintechss and SaaS

| Dimension | fintechss | SaaS |

| AI Applications | Credit, risk analysis, fraud prevention | Automated support, recommendation, optimization |

| Impacts | Financial inclusion, fraud reduction | Customer retention, exponential growth |

| Barriers | Financial regulation, consumer trust | Global competition, cultural adaptation |

| Scaling Strategy | Service democratization | Continuous personalization |

Source: Developed from McKinsey (2023), Mastercard (2022), and WEF (2022).

This comparative analysis shows that AI-mediated scalable innovation is a multifaceted phenomenon: in fintechss, the priority is to build trust in rigid regulatory environments; in SaaS, it is to respond to diverse cultural demands while maintaining technological standardization.

SYNTHESIS TABLE WITH CRITICAL SUCCESS FACTORS

Based on the literature and the documents analyzed, it is possible to synthesize the main factors sustaining scalable innovation with AI in global product platforms. The following Table integrates technological, regulatory, and organizational variables:

Table 3 – Synthesis of critical factors for scalable AI-driven innovation

| Factor | Description | Documentary Evidence |

| Integration into product lifecycle | Application of AI from design through maintenance of digital products | McKinsey (2023) |

| Governance and regulation | Alignment with local and international legislation (LGPD, GDPR, AI Act) | World Economic Forum (2022; 2023) |

| Operational efficiency | Cost reduction and productivity increase via automation and predictive analysis | Mastercard (2022), Boston Consulting Group (2023) |

| Mass personalization | Real-time, user-adapted offerings | Technical reports from Salesforce and Slack |

| Data-driven leadership | Multidisciplinary teams with data-based decision-making | Christensen (2013), Ries (2011) |

Source: Developed by the author based on McKinsey (2023), Boston Consulting Group (2023), Mastercard (2022), World Economic Forum (2022; 2023), Salesforce (2022), and Slack (2022).

This synthesis Table allows us to conclude that scalability in innovation is a multidimensional phenomenon that cannot be reduced to a purely technological perspective. Artificial intelligence is, indeed, a catalytic element, but its real impact only manifests when articulated with solid regulatory governance structures, organizational policies oriented toward ethics, and data-driven leadership.

This articulation promotes not only efficiency gains and exponential growth but also the social and political legitimacy necessary to sustain innovation on a global scale. In other words, AI-mediated scalable innovation requires balancing disruption and responsibility, speed of adaptation and regulatory prudence, exploration of new market opportunities, and preservation of stakeholder trust.

Thus, the results discussed here indicate that the future of digital innovation will not be defined only by the ability to create AI-based products but, above all, by the ability to sustain inclusive, transparent, and resilient global ecosystems. fintechss and SaaS companies, by adopting scalable AI strategies, demonstrate that long-term growth is only feasible when technology, society, and regulation act in synergy. The challenge for contemporary organizations, therefore, is not merely to adopt AI but to do so responsibly, sustainably, and legitimately, transforming technological innovation into social and economic innovation with lasting impact.

FINAL CONSIDERATIONS

This article aimed to demonstrate how the strategic application of artificial intelligence can drive scalable innovation in global digital products, with a focus on the fintechs and Software as a Service (SaaS) sectors. Starting from the central research problem, understanding how AI, in different regulatory and market contexts, acts as a driver of exponential growth, the analysis sought to integrate classical theoretical foundations, documentary evidence, and technical reports of international reference.

The results show that artificial intelligence has consolidated itself as a structuring element of innovation at scale, not only due to its ability to reduce costs and increase operational efficiency but, above all, due to its capacity to personalize services on a massive scale and strengthen the trust of users and regulators.

In the fintechs sector, the relevance of AI in risk analysis and fraud prevention processes was highlighted, favoring the democratization of access to financial services and consolidating competitive advantages over traditional incumbents. In the SaaS model, AI has proven to be an essential condition for sustaining exponential growth, enabling continuous updates, real-time personalization, and customer loyalty across different regions of the world.

From an academic perspective, the study confirms the propositions of Christensen (2013) on the challenges of disruptive innovation, Ries (2011) regarding validated learning, and Tidd and Bessant (2015) on the systematic management of innovation. At the same time, it engages with the contemporary contributions of Andrew Ng (2018), who positions AI as essential infrastructure for all sectors of the economy.

The integration of these references allows us to affirm that the scalability of AI-mediated innovation depends not only on technical advances but also on the organizational capacity to structure governance, ethics, and data-driven multidisciplinary leadership.

Among the practical contributions, the article provides insights for managers of digital platforms seeking to implement AI in their products in a scalable way. The synthesis Tables presented in the previous chapter highlight critical factors that can guide strategic decisions, such as the need to integrate AI throughout the entire product lifecycle, the importance of regulatory compliance in different markets, and the centrality of trust as a competitive asset. For policymakers, the results reinforce that AI regulation must balance innovation incentives and social protection, avoiding both excessive barriers and regulatory gaps that could compromise consumer safety.

In the academic field, the research contributes by systematizing documented experiences in technical reports of reference and articulating them with consolidated theoretical foundations, offering a critical analysis that can support future empirical studies. This contribution is particularly relevant in Latin American countries, where literature on scalable AI-driven innovation is still incipient and lacks studies integrating theory and practice.

Nevertheless, as with all research, this study presents limitations. The main one refers to the absence of primary field data collection, which restricts the analysis to the use of secondary sources. Furthermore, the rapid evolution of artificial intelligence imposes challenges of constant updating, such that the results reflect the state of the art until 2024 but may be surpassed by new technologies and emerging regulations.

In summary, AI-mediated scalable innovation should not be interpreted merely as a technological phenomenon but as a social, economic, and political process that redefines the frontiers of global competitiveness. fintechss and SaaS companies illustrate that large-scale adoption of AI requires a balance between disruption and responsibility, speed of adaptation and regulatory prudence, market exploration, and preservation of trust. The future of digital innovation will, therefore, depend on the capacity to align technology, governance, and ethical leadership, transforming artificial intelligence into collective intelligence in the service of more inclusive and resilient societies.

RECOMMENDATIONS AND FUTURE RESEARCH

The analysis undertaken throughout this article showed that scalable innovation in global digital platforms, driven by artificial intelligence, constitutes a highly complex phenomenon in which technological, regulatory, and social variables intertwine in an inseparable manner. Although the results highlighted critical success factors in the fintechs and SaaS sectors, the challenge remains to transform these findings into practical recommendations and a future research agenda capable of deepening and expanding the debate.

In the field of organizational management, it is recommended that companies operating in global digital environments develop robust governance structures to sustain AI application at scale. This implies not only adopting advanced technologies but also creating multidisciplinary teams composed of professionals in technology, business, law, and ethics. Data-driven leadership should be strengthened through continuous manager training so that strategic decisions are based on evidence rather than solely on intuition or market trends.

From a regulatory perspective, the results suggest that government agencies and supranational entities should advance the formulation of normative frameworks that combine legal certainty, innovation incentives, and consumer protection. The European Union’s experience with the AI Act indicates the possibility of creating proactive regulatory structures that establish transparency and accountability standards without stifling business creativity. In emerging countries, such as Brazil, there is room for research assessing how legislation such as the LGPD can interact with specific AI policies, avoiding gaps that could undermine social trust in digital innovation.

For fintechs professionals, the recommendation is to invest in AI solutions aimed at expanding financial inclusion, focusing on populations underserved by the traditional banking system. This strategy not only ensures competitive advantage but also reinforces the social legitimacy of companies and contributes to reducing inequalities in access to financial services. In the SaaS field, the main recommendation is to prioritize continuous personalization and cultural adaptation of products, ensuring that global solutions are perceived as relevant in distinct local contexts while respecting cultural and organizational specificities.

As for future research, a broad field of empirical investigation is open. Comparative studies between different regulatory markets are recommended to analyze how AI can be scaled in countries with varying levels of institutional maturity. Another promising line concerns the social and ethical impacts of AI-driven scalable innovation, exploring issues such as algorithmic transparency, decision-making biases, and corporate responsibility. Longitudinal studies are also necessary to evaluate the medium- and long-term effects of AI integration in digital platforms, especially regarding economic sustainability and social trust.

Furthermore, the future research agenda should include the analysis of the interaction between AI and other emerging technologies, such as blockchain, quantum computing, and the Internet of Things (IoT), investigating how these convergences may amplify or limit innovation scalability. The integration of multiple technologies could redefine the very notion of global digital platforms, requiring new theoretical and methodological frameworks.

Finally, it is essential that universities and research centers broaden dialogue with companies and regulators, building collaborative agendas that unite scientific rigor and practical applicability. AI-mediated scalable innovation cannot be analyzed in isolation but must be understood as part of a constantly transforming global ecosystem in which science, market, and society must act in an integrated manner.

REFERENCES

BARDIN, L. Content Analysis. Lisbon: Edições 70, 2016.

BOSTON CONSULTING GROUP. The business value of AI: driving innovation and growth in global markets. Global Report. Boston: BCG, 2023.

CHRISTENSEN, C. M. The innovator’s dilemma: when new technologies cause great firms to fail. Boston: Harvard Business Review Press, 2013.

GIL, A. C. Methods and techniques of social research. 7th ed. São Paulo: Atlas, 2019.

LAKATOS, E. M.; MARCONI, M. A. Fundamentals of scientific methodology. 9th ed. São Paulo: Atlas, 2021.

MASTERCARD. AI in financial services: opportunities, risks and governance. Technical Report. New York: Mastercard, 2022.

MCKINSEY & COMPANY. The state of AI in 2023: Generative AI’s breakout year. Global Report. New York: McKinsey, 2023.

MINAYO, M. C. S. The challenge of knowledge: qualitative research in health. 14th ed. São Paulo: Hucitec, 2014.

NG, A. Machine learning yearning: technical strategy for AI engineers. Stanford: Deeplearning.ai, 2018.

RIES, E. The lean startup: how today’s entrepreneurs use continuous innovation to create radically successful businesses. New York: Crown Business, 2011.

SAMPIERI, R. H.; COLLADO, C. F.; LUCIO, M. P. B. Research methodology. 5th ed. Porto Alegre: Penso, 2013.

SALESFORCE. Einstein AI: transforming CRM with artificial intelligence. Technical Report. San Francisco: Salesforce, 2022.

SLACK. The future of work with AI: productivity and collaboration in the digital era. Technical Report. San Francisco: Slack Technologies, 2022.

TIDD, J.; BESSANT, J. Managing innovation: integrating technological, market and organizational change. 5th ed. Chichester: Wiley, 2015.

WORLD ECONOMIC FORUM. Global future council on artificial intelligence and machine learning: responsible AI framework. Technical Report. Geneva: WEF, 2022.

WORLD ECONOMIC FORUM. The future of AI governance: building global trust in artificial intelligence. Technical Report. Geneva: WEF, 2023.